Seritage Growth Properties - Preferred Shares (SRG.PA)

An old idea rears its ugly head (with a twist)

Intro

This is only intended to be a very short write-up reflecting what looks to be an attractive and fairly straight forward asymmetric opportunity. From time to time I flick through Value Investors Club, looking through the most recent ideas under the ‘Highest Quality Idea’ filter. The overwhelming majority of pitches pass straight over my head. Usually they are either too difficult to understand or because I feel there is too much uncertainty to judge the future prospects of the situation and reach a meaningful estimation of fair value (That sadly doesn’t mean I’ve always had the discipline to avoid them). On occasion however, a situation really jumps out off the page, that feels relatively easy to get my head around and where the potential payoff seems highly attractive compared to the risk involved. It reminds me of the Buffett quote from the 1998 Berkshire AGM, where he reminds us that investing is not like olympic diving; there is no ‘degree of difficulty factor’ and as such you do not get a greater payoff for executing a more difficult dive over a simple one. He notes that at Berkshire they look for 1 foot hurdles that they can step over, and tend to not concern themselves with 8 foot hurdles. This feels like a potential ‘1 footer’ and I thank ‘sstrader’ for his writeup on VIC which alerted me to the situation.

Some Background

Feel free to skip this bit of background information on Seritage and jump to the current opportunity section below.

Seritage Growth Properties was originally spun-out of Sears after Bankruptcy and was used as a holding company to house all its commercial real estate assets as well as carrying its large debt load. The company has been on the radar of the value investing communities for a few years as a classic Grahamian net-net opportunity, whereby the asset liquidation value exceeds the market value of the company with a healthy margin of safety. In other words, you are paying cents on the dollar. During Covid, with the ensuing fears surrounding the commercial property market, Seritage’s market value took such a pounding that it reached a level where it was selling for well below an estimate of the net market value of its commercial real estate once you had backed out the debt. Whatsmore, management indicated they were going to pursue a strategy of fully liquidating the real estate portfolio in order to realise this excess value for shareholders.This situation attracted the likes of Mohnish Pabrai and Matthew Petersen. The latter of whom put-out a lot of commentary and information that I found very instructive in forming the foundation for my initial investment back in 2022.

From memory, at the time the company had just over $1bn in debt and Petersen, along with management, had estimated that the net liquidation value per share once they’d paid off this debt was conservatively around the $18 - 30 range. This was at a time where the shares were trading around the $5 - 10 mark. Anyway I made the bet and fast forward a year, Petersen released an interview indicating they had originally grossly overestimated the value of the real estate and their calculations now indicated the liquidation would struggle to realise anything more than $6 - 8 per share. I promptly sold at around $9.5 per share, having recorded a decent gain but more than aware that I had been very lucky and had gotten away with making an array of errors. My learnings were as followed; (1) in these sort of situations a huge margin of safety is a must (2) Always conduct your own work and never purely use someone else's research as the foundation for your thesis (3) Remember in highly leveraged situations, gearing works so that even modest changes in asset valuation can result in far more significant changes in shareholder’s equity.

I took away these learnings and mentally exited the situation with my tail between my legs, feeling extremely fortunate as I watched over the past year as management has repeatedly revised down estimates with the share price tracking down to around $4.5.

With that being said, let's take a look at the present opportunity.

The opportunity

The current opportunity pertains to that of the preferred shares and not the common shares. A class of asset that I must say I completely overlooked in my initial research, and one that has only become recently as the result of some indiscriminate selling as both classes of shareholders reflected their increasing frustration as management delivered further bad news in Q1 2024. Just to give a bit of an overview on preferred shares; the way that capital structure works is such that once the term loan (debt) is fully paid off, additional proceeds will first be diverted to pay off the preferred shares prior to the common shareholders. In other words, during a liquidation, bond holders have first dibs, followed by preferred shareholders, with the common shareholders left to divvy up what's left at the end.

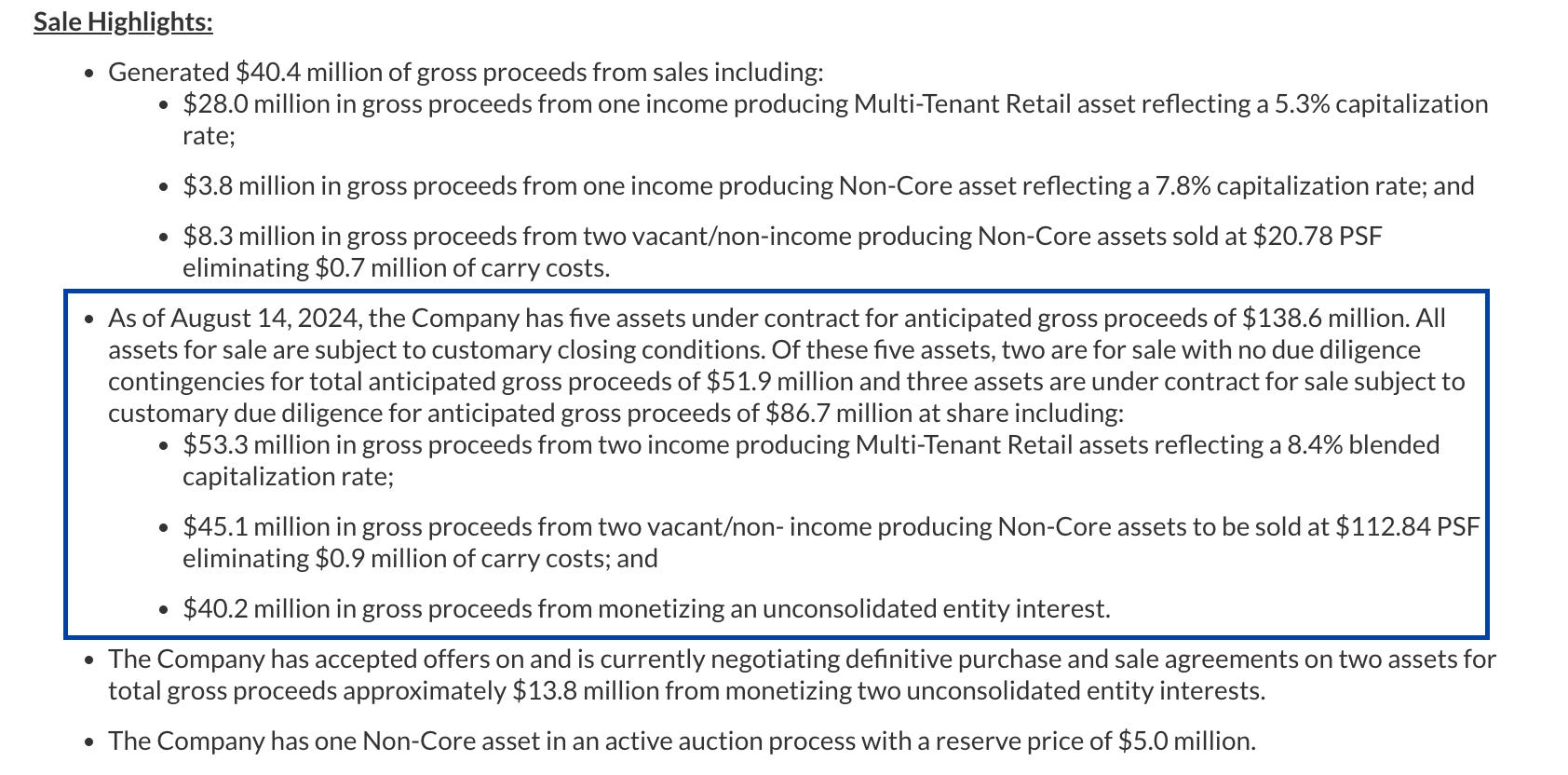

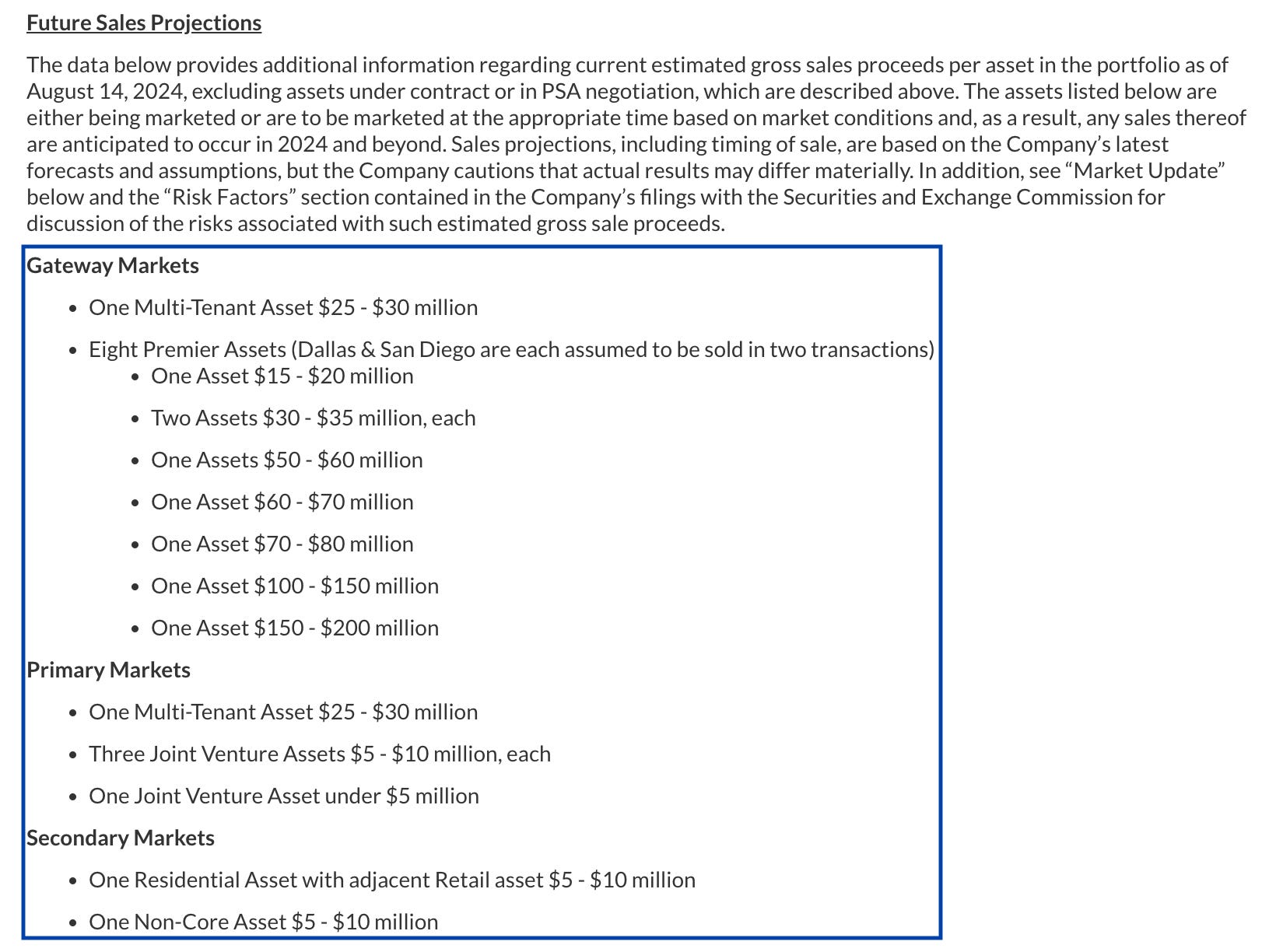

As of the last quarter Seritage had liquidated 87% of the portfolio using the proceeds to pay the term loan down from $1.45bn to $280M. Once this is fully paid off asset sales will then be diverted to the preferred shareholders. With net debt of $200m (as seen in figure 1), current asset sales under contract of $140m (figure 2) and the remaining unsold real estate with an estimated value of $500 - $750m (figure 3). Considering that the total par value for the preferred shares is $70m, there is a near certainty that the preferred shareholders will receive repayment.

Figure 1 - Net Debt

Figure 2 - Sales Under Contract

Figure 3 - Estimated Values of Unsold Real Estate

Of course, you would be right in saying that I’m making the same mistake as mentioned above if I were to take management's estimates at face value again. I feel the difference here is that there is such a large margin of safety and because the ratio of debt to estimated asset value is now lower the negatives affects of gearing are diminished. The estimates would have to be off by over 60% on the downside from a mid range value for the preferred not to be repaid. In other words, if took a mid range value of $600m, knocked off 60% to get $20m, added the proceeds from assets under contract of $140, subtracted a year of cash burn at $80m (OCF has averaged -$20m a quarter) and subtracted net debt from this we still get enough to comfortable repay the $70m preferreds with their dividend attached. (240 + 140 - 200 - 80 = 100). Whatsmore, management has become increasingly conservative with their estimates as they have marked down asset values throughout the liquidation.

Assuming then that the preferreds will be repaid, what does the payoff look like? As seen in figure 4, the preferred shares have a total liquidation preference of $70m. In the event of a liquidation, ‘Liquidation Preference’ is essentially the amount of money prioritised for the preferred shareholders over the common shareholders. Figure 4 also shows there are 2.8m preferred shares outstanding giving them a ‘liquidation preference per share’ or ‘par value’ of $25.

Figure 4 - Equity Structure with the preferred Shares

At the time of writing the preferred trade at $22.50 per share and they also have a $1.75 dividend attached to them paid quarterly. Assuming a 1 year payback - which seems highly attainable given the sales already in the pipeline and the historic rate of repayments - this would generate a 19% return. It's worth noting that at the time of the original write up the preferred were trading at $20 a share which would reflect an even more attractive 34% return. The opportunity reminds me of a Joel Greenblatt quote I saw shared recently;

“If I think I can make 10 times my money that doesn’t make it my favourite investment. If I can invest a lot of money and I don’t see how I’m gonna lose anything, or maybe lose one percent, but maybe I could make five or ten percent that might be a much better risk reward for me.”

I hope you enjoyed this mini writeup. For those interested a full writeup and analysis outlining more information regarding the real estate values and outside risks can be found in sstrader’s original writeup on VIC. Until next time, thanks for reading.