Teqnion...A Compounding Machine? (Part 1)

Read Time | 10 Minutes

Discovering Teqnion (TEQ.STO)

To get going with this blog, I wanted to do a mini series looking at a business I’ve been digging into over the past few months called Teqnion. This first post will give a bit of background as to how I came across the stock, as well as a more general introduction to the business itself. True to the ‘Sit on Your Assets’ approach, Teqnion isn’t a value pick in the ‘traditional’ sense but is instead a potential high quality business trading at a fair multiple. As such, I want to follow this introduction with a more indepth look at different attributes of the business and pinch Chuck Akre’s ‘three legged stool’ framework, breaking the business down into what he sees as the 3 critical components that constitute a compounding machine: ‘Management’, ‘ROIC’ and ‘Runway for growth’.

I Initially came across Teqnion back in November 2022 after seeing a tweet from Chris Mayer indicating he was excited about the business’s long term prospects and as such had made it a position in his fund, Woodlock House Family Capital. Mayer had recently hit my radar after picking up his super book ‘100 baggers’, where he looks at the highest returning stocks over the past few decades and helps shed light on the early traits an investor can look for in a business with the potential to return that illusive 100X. Mayer is what you would have to call a hyper-inactive investor, suggesting last year's one sell and one buy decision was a ‘busy year trading’. It goes without saying that he has an extreme focus on quality and that there is an extremely high bar for new businesses to get into his portfolio, which is why any new purchase is pretty intriguing and his recent purchase of Teqnion was sure to pique my interest.

Puppies but not Unborn Puppies

Some further digging into Mayer’s portfolio not only showed it was his most recent purchase but also revealed it was by far the smallest market cap in the fund at $272M (table from @bkaellner). This inherently makes it more intriguing as it indicates there may be an opportunity to get into a high quality compounder at an early stage of its lifespan, giving the a greater opportunity for an attractive upside potential. In addition to being relatively small, Teqnion has also had the opportunity to create a fairly substantial 16 year track record, demonstrating key attributes such as capital allocation, stability, and cash flow growth. Mayer highlights this point in ‘100 baggers’ where he discusses the idea of looking for ‘puppies’ but not ‘unborn puppies’. This, in essence, is the balance between finding businesses with a big enough runway ahead of them to compound long into the future, and a material track record, demonstrating the business’s performance. This is by its very nature pretty difficult to find, as normally by the time management have built up a big enough track record and you've caught wind of what is an exceptional business, either the universe for future high return investment opportunities has significantly shrunk or the price has been bidded up in the market to a point where returns no longer look attractive. As such, I think finding Teqnion at a point where it falls into this sweet spot and trades at a not too outrageous multiple of a PE of around 25 (although it recently expanded to 33), could potentially be quite interesting and I therefore think it worthwhile to dig a little deeper into their DNA and find out what Mayer is excited about.

Teqnion in a Nutshell

Based in Solna, Sweden, Teqnion is a serial acquirer with a focus on purchasing industrial groups that are market leaders in the specific industrial niche in which they operate. Established in 2006, Teqnion currently has 25 of these daughter companies with 22 in Sweden, 2 in the UK and 1 in Ireland. They have a total of 465 employees throughout these daughter businesses with a small team of just 7 employees at the mother company. They currently have a market capitalisation of 3.79B SEK, revenue of 1371M SEK and net earnings of 112M SEK (you can divide by 10 to roughly get these into USD).

Teqnion focuses on fairly small businesses usually in the region of $3M to $15M in annual sales. They finance their deals with 50 percent cash and 50 percent debt with an emphasis on acquiring businesses that either sell or service physical products. Johan Steerne, CEO and cofounder, feels that these industries are less likely to be disrupted by digitisation, and that the pace of change in these un-sexy, non-faddish industries is generally slower, giving them greater confidence in the enduring value of the businesses they acquire. I won’t do a full rundown of the daughter companies, as they can be found on the website, but they sell a diverse range of products including electric wheelchairs, various other electronics, hydraulic components, house building, maintaining gas turbines, steel systems for professional kitchens, catering trucks, fluid dispense pumps, weighing scales, protective vehicles, military combat training equipment and many more. Management often talk about the idea of standing on many legs and how that enables them to create a more stable and enduring platform, from which to grow steadily over time. Daniel Zhang, CXO speaks to this idea, saying “Teqnion is built on the idea that it will never be the one to grow the fastest, not all the companies will be performing at their top level at the same time, but it will also hopefully never fall apart as we have things that will go better in recessions as well”.

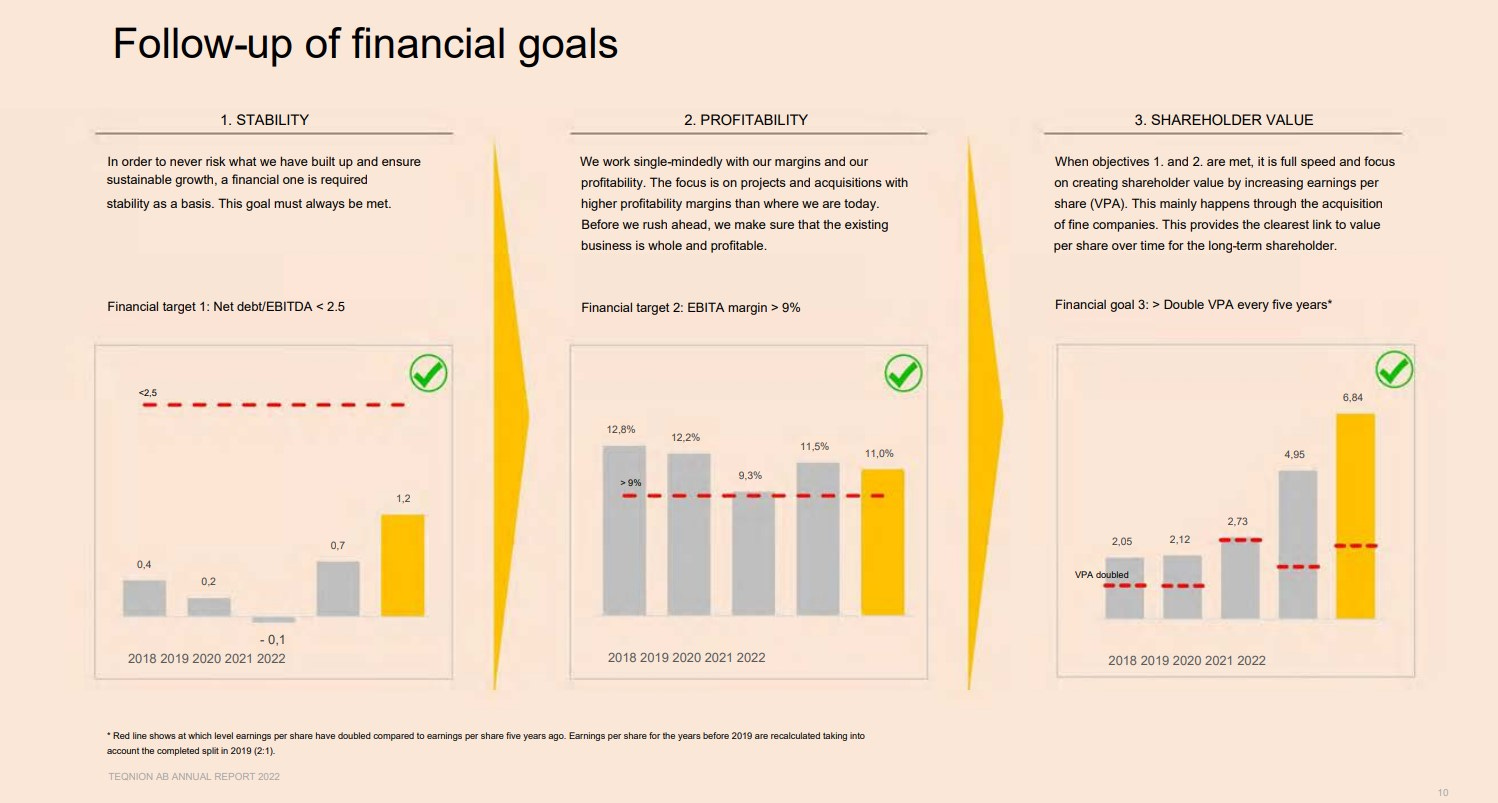

Teqnion’s 3 Pillars

Stability is in fact the first of Teqnion’s three key performance indicators that they use to measure their progress overtime, the other two being profitability and shareholder value (See the graphs from their annual report below).

Stability not only points to diversity but also the focus on not overstretching themselves by employing excessive amounts of debt at any one time and keeping the debt/EBITDA ratio to below 2.5x. They avoid making large leaps of faith with big ‘make or break’ acquisitions and have no appetite for risky purchases that have the allure of rapid growth but may leave the business in a more fragile positions and financially vulnerable in the event of any underperformance or unforeseen headwinds. In the latest annual report, Johan alludes to the idea of taking millions of ant steps towards infinity, and I feel this nicely exemplifies management’s philosophy of allowing the acquisition rate to increase organically, commensurating in line with their ability, as they make more deals and grow knowledge and experience over time.

The second of Teqnion’s pillars: ‘Profitability’, puts focus on the free cash flow margin, ensuring they are healthy and above 9%. Johan and Daniel often talk about how for them as serial acquirers, cash is the raw material they need in order to grow. They run a very lean operation at HQ (reminiscent of what I’ve read about Tom Murphy at Capital Cities) and are very cost conscious, being very candid about the fact that they are a non revenue generating part of the business. They are also focused on sustainably increasing profit margins at the daughter companies which is normally in the low single digits and is the first engine in what management describe as Teqnion’s twin engine growth. Any excess cash that isn't able to be redeployed at high returns within the daughter companies is sent back to HQ, where Johan and Daniel try to allocate it effectively by acquiring more new, nice, high quality companies. This is the second, and somewhat larger engine for growth, as is the blueprint for the serial acquirer that they aim to repeat over and over.

Over time, this is how management aims to achieve the third and final KPI, which is creating shareholder value. Management has a very strict approach to valuation that they have had from the start and it helps them make sure their acquisitions create value as opposed to destroying it. They have the simple framework of wanting to get their money back from the business they acquire within 5 years of the purchase. This of course means paying roughly a 5x multiple for any business with no growth prospects but paying a proportionally higher multiple if they feel the opportunity for growth is greater. Teqnion make it very clear that they will oftentimes not be the highest bidder. Instead their acquisition model works (and this is really at the core of the business’s DNA) on the idea that they will be a trustworthy mother company and a safe harbour for the entrepreneur’s business that he or she is selling, treating existing employees with respect and preserving the company's culture. If sellers equally value these things ahead of just money, then Teqnion creates this sort of self selecting process where they can pay less to purchase companies that also put value on these softer sides of business. Management are focused on building their reputation as attractive buyers and in reality rarely have to bid competitively for companies as they develop long standing relationships with potential sellers, manifesting a web of trust between daughter company CEOs. Overtime, they hope to build this network out and compound the benefits of goodwill, similar to their idols at Berkshire Hathaway. As seen at Berkshire, a favourable reputation can act as a very wide and enduring moat, that combined with prudent capital allocation, provides a very potent recipe for success. Daniel has spoken about his ambition to double EPS every 5 years and as such over a 50 year time horizon create a 1000x return for the longterm Teqnion shareholders.

With that being said, I hope you enjoyed this short overview of Teqnion and have gotten a bit of flavour for what the business is about and is aiming to achieve. I hope to catch you in the next post where we’ll dig a little deeper into Teqnion’s management.

Thanks for reading and make sure to share and subscribe if you enjoyed this.

cheers for now.